DATA 622 Meetup 6: Resampling

2026-03-03

Week Summary

- Groups: Email me your members asap, also set up time to meet

- If not in a group, email me immediately if you want to get a grade for the proposal

- HW 4 available- it involves lots of reading but not as much work as it looks

- Chapter 5 of ISLP

Events

![]()

nyhackr.org

Events

- Data Science Seminar with Jiahao Chen

- Director of AI/ML at NYC Office of Technology

- Wednesday, March 25th at 6:30PM

Train-Test Redux

- Goal of Predictive Model Selection:

Best out of sample performance

- Hold out data for testing

![]()

Train-Test Redux

- If you are comparing many different models and features, sometimes need three datasets

![]()

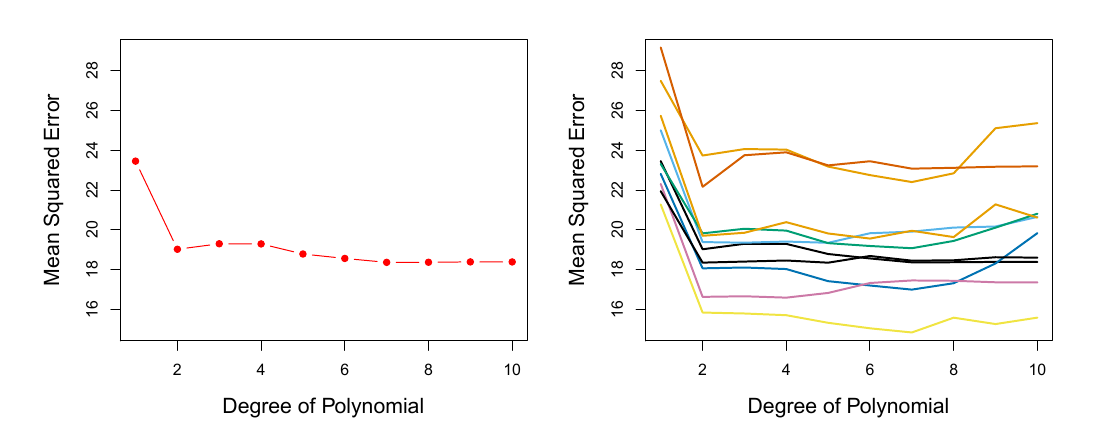

Train-Test Split Problems

- Estimate of out of sample performance has high variance due to single split

![]()

ISLP 5.2

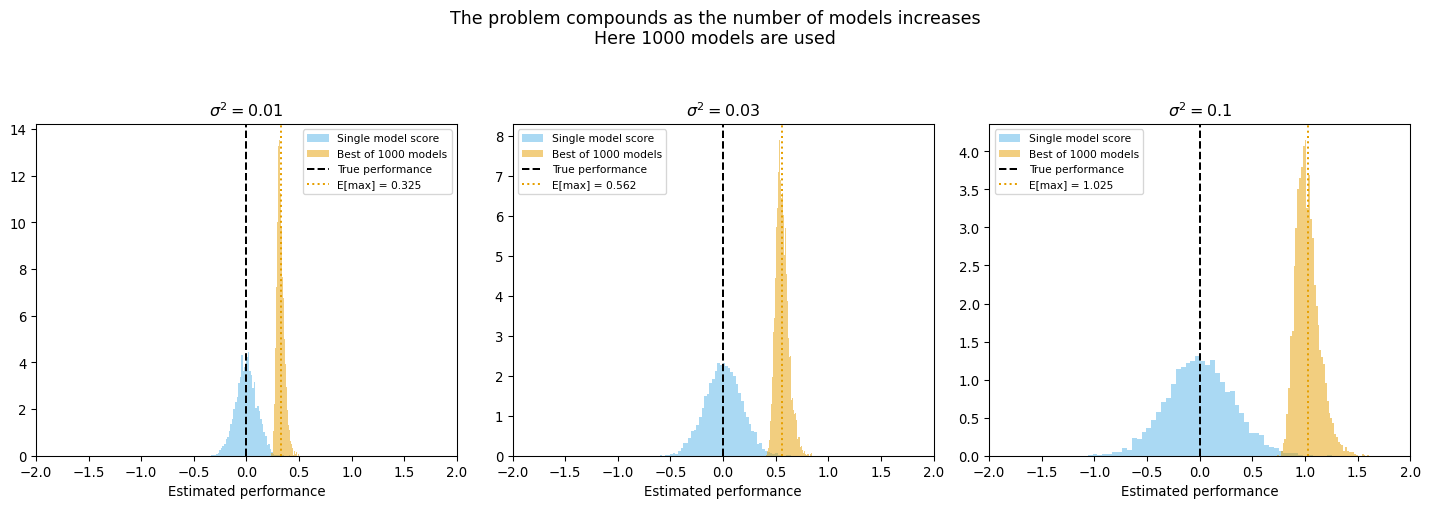

Train-Test Split Problems

- High variance compounds multiple-comparison issue

![]()

Train-Test Split Problems

- High variance compounds multiple-comparison issue

![]()

Train-Test Split Problems

- Estimated accuracy is based on a model fit to less than the full data

- Can lead to understimated accuracy

- Data Inefficient

- Sensitivity to rare classes

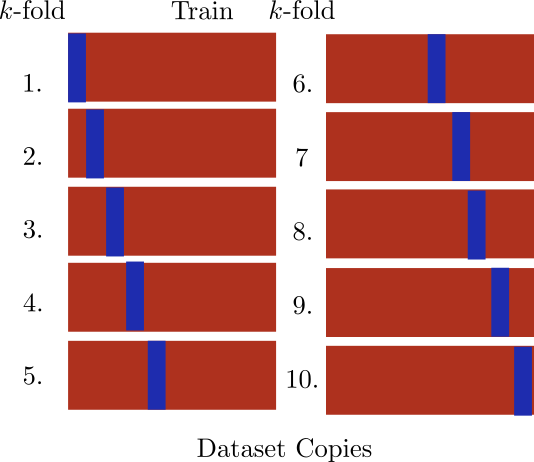

Cross Validation

- Cross Validation divides data into “folds”

- Fit on \(k-1\) folds

- Estimate error on \(k\)th fold

- Repeat and then average

Cross Validation Disadvantages

- You have to fit your model multiple times (potential dealbreaker)

- How accurate is your estimate of accuracy? Now it is subtle

- Data leakage issues are more subtle

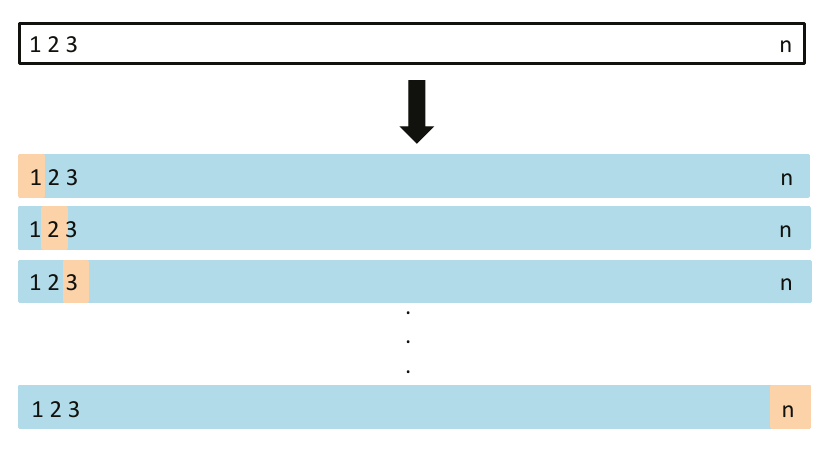

Leave One Out Cross-Validation (LOO-CV)

- Each “fold” has a single point

- Train entire model on \(n-1\) points, test on \(1\), repeat

![]()

LOO-CV Tricks

- Refitting model over and over sounds horrendous… but,

- There are tricks to get ‘LOO-CV’ for free

Linear Models

\[

\mathrm{CV}_n = \frac{1}{n}\sum_{i=1}^n \frac{\left(y_i - g_{\mathrm{full}}(\mathbf{x}_i)\right)^2}{1-h_i}

\]

- Leverage \(h_i = \mathbf{x}_i^T(X^TX)^{-1}\mathbf{x}_i\)

LOO-CV Tricks

- Refitting model over and over sounds horrendous… but,

- There are tricks to get ‘LOO-CV’ for free

Linear Models

\[

\mathrm{CV}_n = \frac{1}{n}\sum_{i=1}^n \frac{\left(y_i - g_{\mathrm{full}}(\mathbf{x}_i)\right)^2}{1-h_i}

\]

- ‘sklearn’s ’RidgeCV’ does this automatically

LOO-CV Tricks

- Refitting model over and over sounds horrendous… but,

- There are tricks to get ‘LOO-CV’ for free

Bayesian Models

- This can be approximated for any Bayesian model using Pareto Smoothed Importance Sampling

- See the arViz package

k-Fold Cross Validation

- For \(k\)-fold, error estimate is:

\[

\mathrm{CV}_k = \frac{1}{k}\sum_{i=1}^k \mathrm{MSE}_k

\]

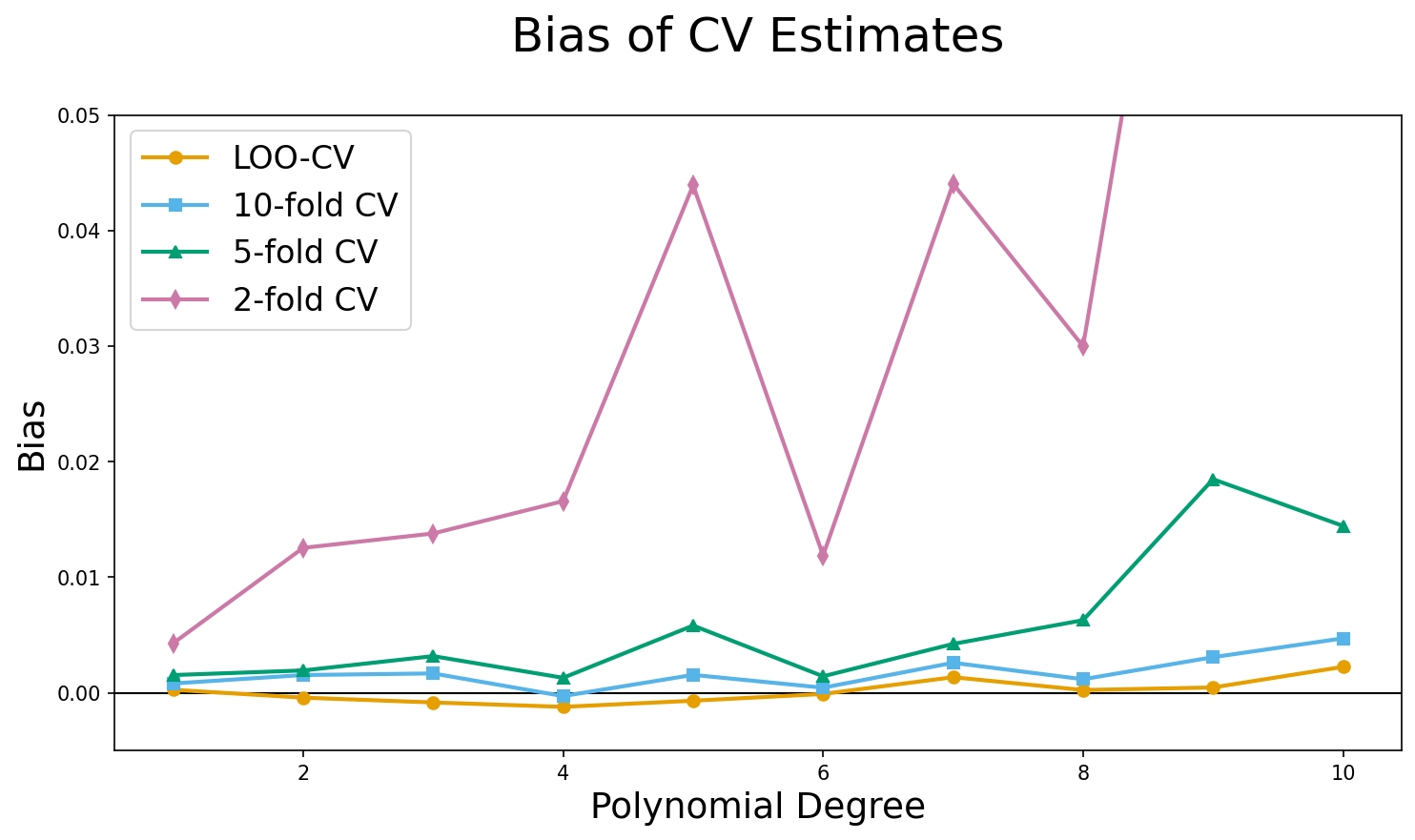

How many folds?

- ‘LOO-CV’ is least biased

- Because it uses more data per model, the models are closer to the full model

![]()

How many folds?

![]()

- Your textbook argues that “variance” increases with \(k\), in a kind of bias-variance trade-off

- But they don’t give any evidence

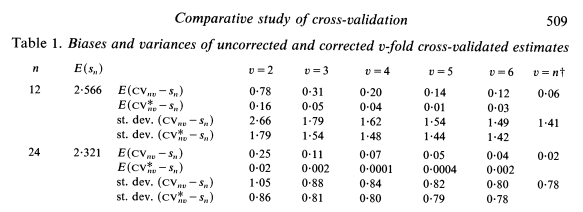

How Many Folds?

- It has been proven mathematically at least for linear regression, that there is no trade-off!

- ‘LOO-CV’ has lowest variance and lowest bias

![]()

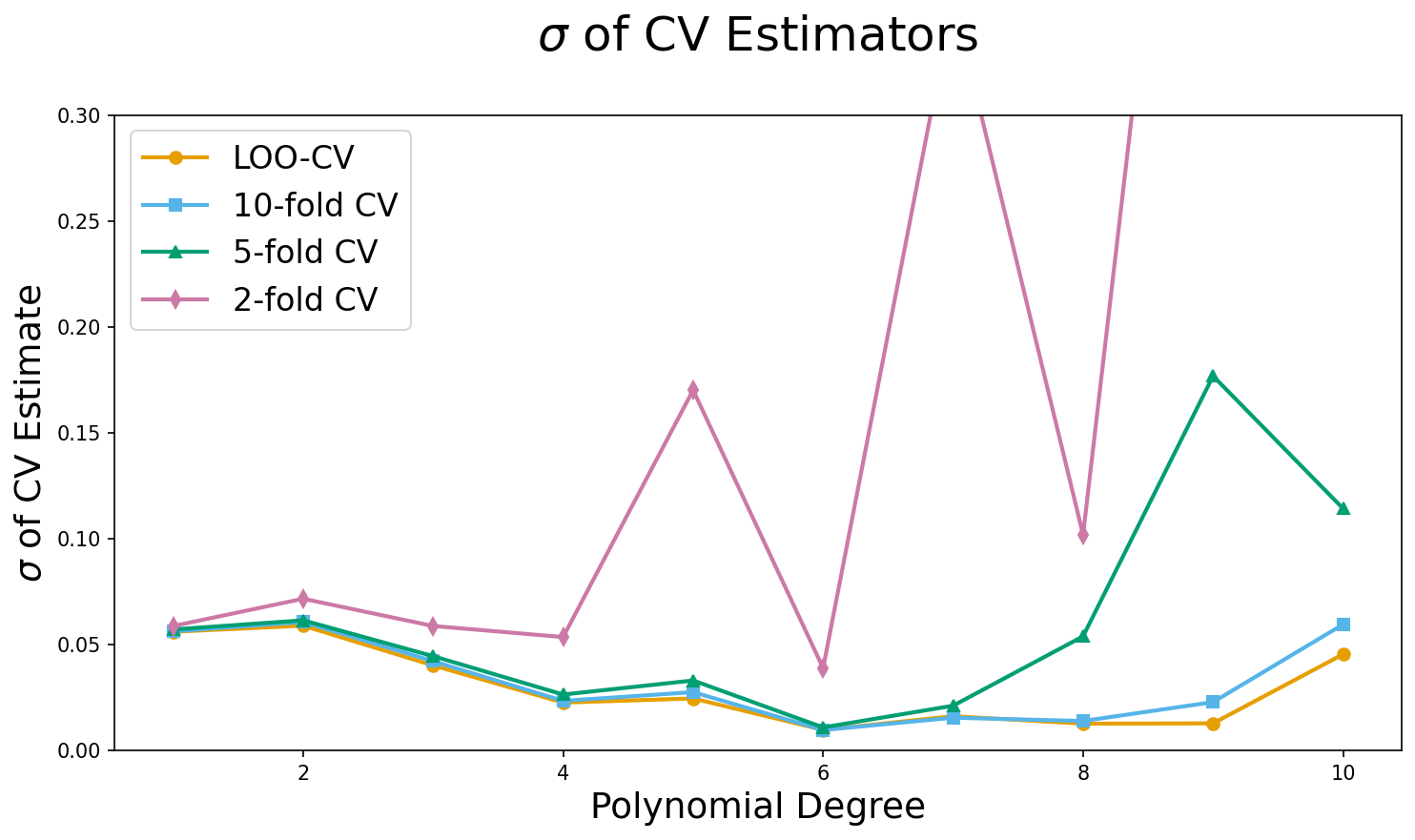

‘LOO-CV’ variance?

- I tried it with repeated experiments using known data generating process

- ‘LOO’ is best

![]()

How Many Folds?

- Decide based on how much data you have and if you have a fomula to get ‘loo’

- \(k=5\) is a bit more than 5x

- Difference to ‘loo’ is proportional to your data

- At same time, bias and variance advantages of ‘LOO-CV’ decrease with more data

Validation, k-fold or LOO-CV?

- If you have no other choice, validation

- If you can, ‘LOO-CV’

- Otherwise, \(k=5\) is a great choice that is a sweet spot of computational expense and diminishing returns to bias and variance

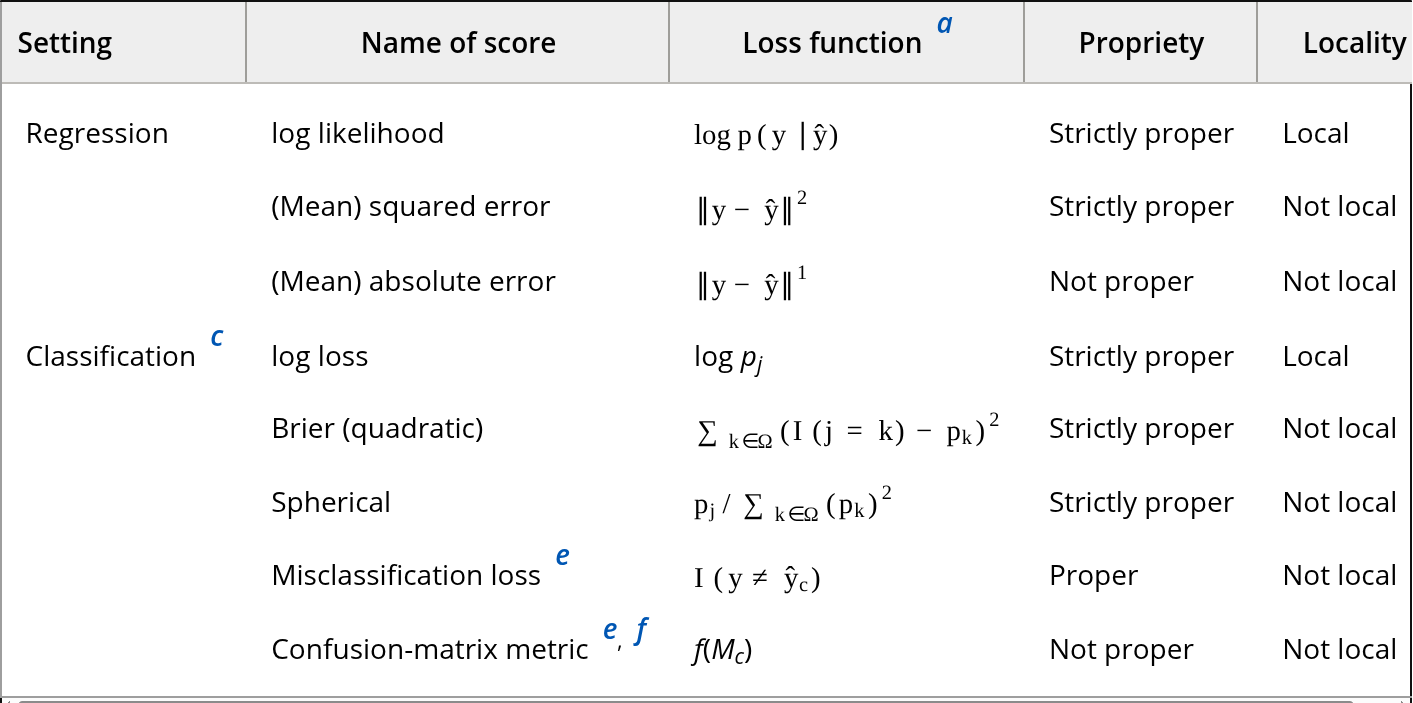

What Metric to Use?

![]()

Yates 2022 et al

Proper and Local Metrics

Proper Metric: This is one where if your model was the data generating process it would be scored highest

Local Metric: For each observation, contribution to score only rates to probability of predicting correct class

Metric Selection Advice

- If you have likelihood, use ‘log’ scoring

- Both classification and regression

- If costs are well known, you can construct a custom metric based on that

- If ranking is key, AUC of ROC curve or similar is not bad

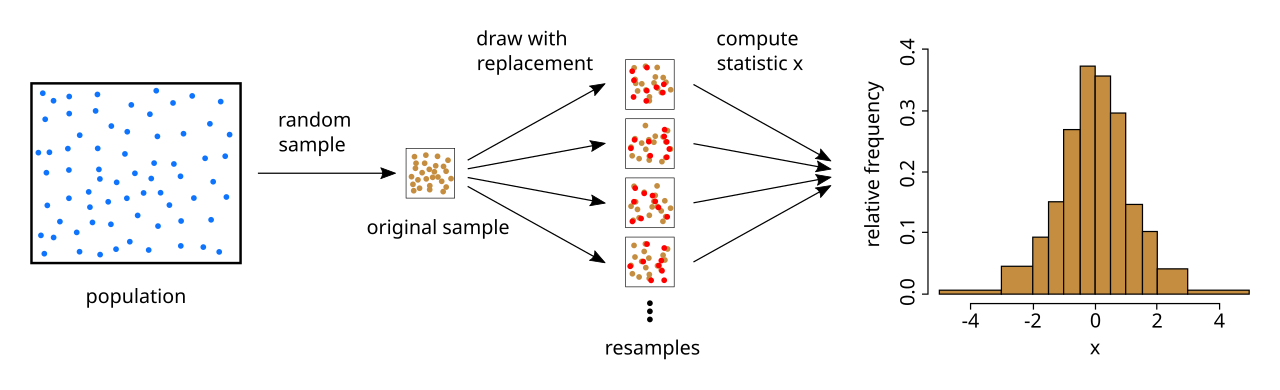

The Bootstrap

- Motivation: For complicated models there aren’t “statistics” we can use to derive uncertainty estimates

Bootstrap: Create a lot of fake datasets by resampling from your data with replacement

- Get “samples” from your model, empirical confidence intervals

The Bootstrap

![]()

wikipedia

The Bootstrap

- Resample “B” times, coefficient or prediction \(c_r\) for each boostrap \[

SE_{c} = \left(\frac{1}{B-1}\sum_{r=1}^B\left(c_r - \bar{c}\right)^2 \right)^{1/2}

\]

Bootstrapping is Expensive

- Convergence rate is \(\frac{1}{\sqrt{B}}\)

- Slower for tails, need more reps for confidence intervals

- Main use cases are complicated, but not computationally intensive models

- Various types of regression

- Tree based methods (“bagging” is based on bootstrap)

No Inference after Model Selection

- Suppose you care about the values of the model coefficients

- You have a family of different models, and you use cross-validation to pick the “best” one

- Then you look at the model coefficients of the best model

- Smart?

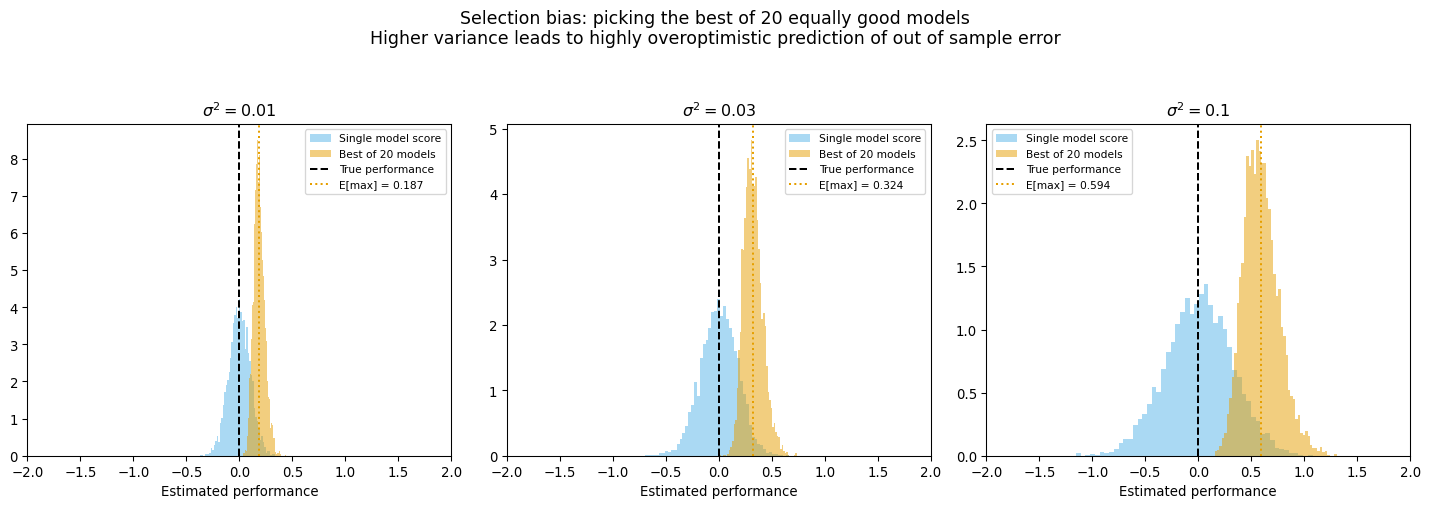

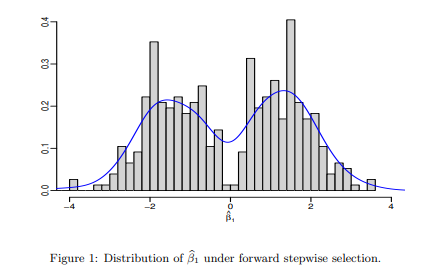

No Inference after Model Selection

- Winner’s Curse- winning model will only include features with a high coefficient

- Values biased away from 0 and standard errors biased low

![]()

Bias Correction

- Cross-Validation penalizes more complex models because smaller than full dataset is used

- If \(S_g\) is the score of a model \(g\), the bias correction is:

\[

S_g^* = S_g +\frac{1}{n}\sum_{i=1}^n \nu_i, \\

\nu_i = L(y_i,g(\mathbf{x}_i)) -\frac{1}{k}\sum_{j=1}^k L(y_i,g_j(\mathbf{x}_i))

\]

One Standard Error Rule

- Overfitting is something that can occur in model selection

- When you compare a lot of models, the ones that get selected have all there variables as important, some due to chance

![]()

One Standard Error Rule

- Compute standard error of Score estimate of best model: \[

SE_{CV} = \frac{\hat{\sigma}}{\sqrt{n}}

\]

- Pick simplest model with CV score within one standard error of the best model average